S&P 500 Growth No Longer Requires Job Growth: The Decoupling Era Has Arrived

- Bella Battsengel

- 12 hours ago

- 8 min read

We are seeing a historic decoupling where S&P 500 growth no longer requires job growth. Innovation is rewriting the rules of the global economy.

For decades, S&P 500 performance and job growth were twins. They moved in lockstep. When companies grew revenue, they hired people. When they expanded markets, they expanded teams. Economic growth meant employment growth.

That bond is breaking. We are entering the Decoupling Era.

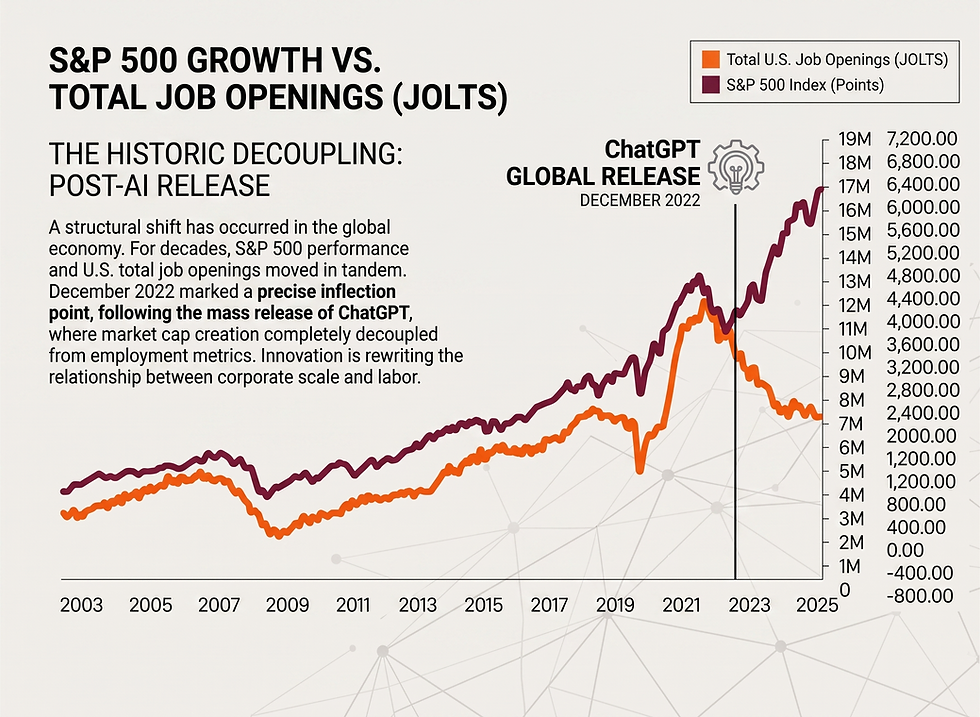

The Data That Changes Everything

A chart emerged recently showing S&P 500 companies experiencing record growth whilst simultaneously reducing headcount and job openings. This is not a temporary anomaly. This is a structural shift.

The inflection point was December 2022. The month after ChatGPT released. The transformation started happening instantly. That is the power of AI and the acceleration it brings to the five platform technologies converging simultaneously.

What Historic Coupling Looked Like

Traditional economic theory held that company growth required proportional workforce expansion. A company doubling revenue needed to roughly double headcount. Productivity gains existed but were incremental. Technology improved efficiency but did not eliminate labour requirements entirely.

This created predictable patterns. S&P 500 growth drove employment. Employment drove consumer spending. Consumer spending drove economic growth. The cycle reinforced itself.

Investors could rely on this coupling. Growth companies were job creators. The companies scaling fastest were hiring fastest. Headcount growth signaled business momentum.

What the Decoupling Actually Means

Through AI, robotics, and digital human emulators, companies are now scaling revenue whilst keeping headcounts lean. It is a paradox. Productivity is soaring, but the traditional job is being redefined in real time.

The Mechanics of Decoupled Growth

Companies are achieving revenue growth through three primary mechanisms that do not require proportional headcount expansion.

AI automation of knowledge work. Tasks that previously required human analysts, coordinators, and administrators now run through AI systems. Customer service. Data analysis. Content creation. Report generation. These functions scale without scaling teams.

Digital human emulators. XAI was reportedly trialing AI that emulates how humans engage with computers. Typing. Mouse clicks. Browser navigation. These emulators were placed on the org chart. AI employees performing actual work previously done by humans.

Agent-to-agent infrastructure. Google released their AP2 protocol for agent-to-agent payment rails. Secure crypto payments between AI agents. The future of business looks like agents dealing with each other and operating with each other. No humans required for the transaction layer.

The Australian Context

The Australian private market raised $224 billion in 2025. But unemployment concerns are rising despite economic growth. The decoupling is not just a US phenomenon. It is global.

Australian employment laws are becoming increasingly difficult to manage. Workers compensation claims where 38% relate to mental health issues rather than physical workplace problems. Right to disconnect laws making it difficult for companies with international ambitions. Firing and redundancy laws creating almost impossible barriers.

The result is companies have no incentive to hire in Australia. The combination of regulatory burden and AI capability makes headcount reduction the rational choice.

The AI Acceleration That Enabled This

AI is not overhyped. The acceleration of AI has been bottlenecked. Until those bottlenecks lifted, the full potential remained constrained.

The Bottlenecks That Delayed Decoupling

TSMC packaging and advanced packaging concerns created deployment delays from 2023 to 2025. TSMC was pragmatic about infrastructure investment. They did not want to overbuild for demand that might disappear. Infrastructure requires years to build.

Blackwell delays from Nvidia created unexpected software innovation. Companies waiting for next-generation chips started adding software layers over existing models. Reasoning capabilities. Deep research functionality. Agentic use cases. These software advances happened because hardware delays forced alternative approaches.

High bandwidth memory shortages prevented GPU speeds from reaching full potential. Production lines could not scale fast enough to match demand.

The power wall. Chips sitting idle in warehouses because power infrastructure cannot support them. The US is now providing permissions for tech companies to build power stations on the same sites as data centers.

What Happens When Bottlenecks Lift

2026 is the true AI acceleration year. Hardware bottlenecks are being lifted. Vera Rubin platform from Nvidia delivers five times the inference at ten times lower token cost versus Blackwell. This will power agentic reasoning and long context models.

Whole new potential gets unlocked. Agents explode. Progress surges. Massive competition both in the US and China plus geopolitical competition creates the foundation for acceleration.

When the bottlenecks lift, the decoupling accelerates. Companies that were constrained by AI capability limitations suddenly have unlimited automation potential.

The Entry Level Job Crisis

Entry level roles are being wiped out. This was predicted. This is ongoing. The greatest concern in the market is the reduction in jobs available for entry level positions because AI is playing such a significant role.

The Middle Management Acceleration

The last three years focused on wiping out middle management. That has been continuing. Now there is significant job reduction in entry level availability.

But the most important pattern to note is the historical decoupling of growth and employment. S&P 500 companies growing whilst reducing headcount and job openings.

This transformation started December 2022. ChatGPT release month. The coupling that existed for decades broke instantly.

What This Means for Career Pathways

Traditional career progression assumed entry level positions led to middle management roles led to senior leadership. Each step required demonstrating capability in the previous role.

When entry level positions disappear, the entire pathway collapses. How do you develop middle managers if no one gains entry level experience? How do you identify future leaders if the proving ground does not exist?

Companies are not solving this problem. They are accelerating it. Every AI capability deployed eliminates more entry level work. The capability gap widens between what new graduates can do and what companies need.

The Productivity Paradox

AI creates a productivity paradox. Eight hours of work compressed into five hours. Does this lead to four-day work weeks? Does the traditional 9-to-5 become 10-to-3?

What will people do with the time AI gives back? The thesis from major AI allocators is food, nature, and sport. Human beings want to be entertained. We are not all going to sit around contemplating our navels, writing poetry, and reading philosophy.

The Second Derivative Investment Thesis

A US fund manager heavily allocated to OpenAI and Anthropic explained their thinking. "We are about as allocated to directly to artificial intelligence as we possibly can be. What we are starting to look at now is the second derivative benefits from that technology if our original thesis is correct."

Attention and content become the business. Sports and entertainment capture time that AI liberates from work. This is the macro investment thesis driving capital into assets that benefit from increased leisure time.

But this assumes displaced workers find alternative income sources. If AI eliminates jobs faster than new opportunities emerge, people have time but no purchasing power. The entertainment economy collapses without income to fund it.

The Investor Question: Old World or New World?

As investors, we have to ask: Are we backing the old world of labour-intensive growth, or the new world of high-margin, automated abundance?

Old World Economics

Old world companies scale revenue by scaling teams. Headcount growth signals business momentum. Human capital is the primary input. Labour costs are the primary expense. Growth requires geographic expansion to access talent pools.

These companies face margin compression as they scale. More people means more complexity. More HR overhead. More management layers. More office space. More everything.

Valuation multiples reflect this reality. Revenue per employee becomes a key metric. Companies with higher revenue per employee trade at premium multiples because they demonstrate efficiency.

New World Economics

New world companies scale revenue without scaling teams. AI agents are the primary input. Infrastructure costs are the primary expense. Growth requires compute capacity, not talent pools.

These companies face margin expansion as they scale. AI scales without proportional cost increase. No HR overhead per additional agent. No management layers. No office space. Infrastructure costs decline per unit as volume increases.

Valuation multiples will need to adjust. Revenue per employee becomes meaningless when employee count is intentionally minimised. Revenue per dollar of infrastructure spend becomes the relevant metric.

The Allocation Implication

Capital allocators must choose. Back companies hiring aggressively to fuel growth? Or back companies deploying AI to fuel growth without headcount?

The former looks like traditional investing. Familiar metrics. Proven playbooks. Understandable risks. But potentially obsolete business models.

The latter looks like venture into uncharted territory. New metrics. Untested playbooks. Unknown risks. But potentially the only sustainable business models going forward.

According to recent surveys, 42% of family office portfolios have shifted into alternatives. Alternatives have become the main event and the primary engine for capital appreciation. The shift to AI-enabled, headcount-lean businesses will accelerate this trend.

The Australian Private Market Implications

Australia represents 0.3% of world population but generates 3% of global research output. Cochlear implants. Wi-Fi. HPV vaccine. World-class innovation capability exists.

But Australia also has 141,484 startups with only 10,200 securing funding. A 93% failure rate in capital engagement. The infrastructure connecting founders to capital is broken.

The Decoupling Opportunity

The decoupling creates opportunity for Australian companies that can scale without proportional headcount growth. Regulatory burden around employment becomes irrelevant if you are not hiring.

Australian businesses that leverage AI to achieve growth without headcount expansion can compete globally without the traditional disadvantages of distance, labour costs, and market size.

But this requires capital allocators to recognise and fund these business models. To accept that headcount is not a growth signal. That lean teams are not a weakness signal. That AI infrastructure spend is equivalent to talent acquisition spend in old world models.

The Infrastructure That Enables This

CapitalHQ exists because capital engagement infrastructure is broken. Founders spend 80% of their time on manual investor relations. Investors drown in fragmented deal flow. The system does not scale.

The decoupling era demands infrastructure that scales. Always-on investor relations that does not require proportional human effort as portfolio size grows. Intelligent deal flow filtering that surfaces high-signal opportunities without human screening of every submission.

This is not optional. This is the same shift happening across the entire economy. Manual processes being replaced by intelligent infrastructure. Human effort focused on high-value activities that AI cannot yet perform.

The Future That Arrives in Months, Not Years

The Big Bash League privatisation happens June-July 2026. Teams like Sixers, Scorchers, Renegades, Stars will go for prices that make people's eyes water. Particularly if IPL owners compete with local syndicates.

This is the near-term catalyst. The market waking up to how underpriced and misunderstood sports and entertainment assets are in the decoupling era.

But the broader pattern is clear. We are not waiting five years for the decoupling to materialise. It has already started. December 2022 was the inflection point. Everything since is acceleration.

What Founders Must Understand

If you are building a business that requires proportional headcount growth to achieve revenue growth, you are building an old world business. Investors will increasingly question whether that model can compete.

If you are building a business that leverages AI to scale revenue without scaling teams, you are building a new world business. But you need to articulate this clearly. Investors still pattern-match to old world metrics.

The capability to tell this story becomes critical. Not just "we use AI." Everyone uses AI now. But "our business economics improve as we scale because AI handles functions that traditionally required linear headcount growth."

What Investors Must Understand

Companies reporting headcount reductions whilst growing revenue are not in distress. They are adapting to new economic reality. This is not cost-cutting. This is structural business model evolution.

The metrics that worked for decades are breaking. Revenue per employee becomes meaningless. Headcount growth as momentum signal becomes obsolete. New frameworks are required.

The investors who adapt fastest will capture disproportionate returns. The investors who cling to old world metrics will systematically mis-allocate capital into obsolete business models.

The Cold Reality of the Decoupling Era

S&P 500 growth no longer requires job growth. Innovation is rewriting the rules of the global economy. This is not coming. This is here.

The question is not whether the decoupling will happen. The question is whether your capital allocation strategy accounts for it. Whether your portfolio is positioned for old world labour-intensive growth or new world high-margin automated abundance.

The Australian private market raised $224 billion in 2025. Capital exists. But it will flow to the business models that align with new economic reality, not the models that worked for the past 50 years.

For founders, the imperative is building businesses that scale without proportional headcount. For investors, the imperative is recognising and funding these models before multiples adjust to reflect their structural advantages.

For everyone else, the imperative is understanding that the traditional job is being redefined in real time. The coupling that connected economic growth to employment growth has broken. What replaces it determines the shape of the next decade.

We are not watching the birth of a new economic law. We are watching the death of an old one. Those who adapt win. Those who cling to outdated assumptions lose.

The decoupling era has arrived. Position accordingly.